When someone is diagnosed with an aggressive illness, such as mesothelioma, finding effective medical treatment is naturally the first thing on the patient and their family’s minds. While health and wellness deserve the highest priority, financial planning plays a larger role in cancer treatment than many people realize.

Financial toxicity happens when the cost of mesothelioma care causes stress and problems beyond medical bills. For many people, the financial burden reaches far beyond what insurance covers.

The key to effective financial planning is to do it early. The best time for financial planning is before beginning treatment and before the cancer progresses any further.

Financial Planning Tips

Ask about the costs of treatment and any available alternatives.

Be proactive in searching for financial help with medical bills.

Designate a trusted caregiver to help with important decisions.

Examine the details of health insurance coverage closely.

Research finds financial responsibilities influence patients’ priorities and affect treatment decisions. The rising cost of mesothelioma treatment is a complex problem, but people can take steps to reduce financial stress. The key is to plan early before mesothelioma treatment begins and before cancer progresses, so patients and families can focus on care rather than costs.

Exclusive Content

| Patient Story: Financial Burden of Mesothelioma

There’s a lot of unexpected that can come with any cancer diagnosis, especially mesothelioma, whether that be home medical costs, an unexpected trip to the emergency room. A patient shouldn’t have to make a decision about the treatment they’re going to have or traveling to a center of excellence based on affordability.

We didn’t know what mesothelioma was. Of course, we looked it up on the phone. It didn’t look good.

We were facing a lot of financial problems during that time. We were not prepared for it, all the medical bills, and then we had to travel. We don’t live in Houston, so we had to travel back and forth. And then he had to go into short term disability.

And my job, of course, I don’t earn a lot of money. So it was kind of hard to do all that.

The average mesothelioma patient is typically retired. So usually they are on Medicare, which means that there is twenty percent out of pocket. So when a patient is receiving a form of systemic therapy, they can anticipate a couple thousand dollars per infusion.

I have not reached a point yet where I don’t continue to have a lot of doctor visits, lot of medical bills, and the cost of insurance, the deductibles, and all of these things, they continue.

What I do regret is not spending more time with him when we got home because I had to work. I had to work two jobs to pay the bills.

Navigating the financial options on your own can be super overwhelming. First of all, you’re dealing with a diagnosis that can be very expensive. Oftentimes, you don’t know if your insurance is gonna pay for your healthcare. Are you gonna be able to afford your co pays? What is it gonna look like in six months or a year from now? We actually have learned all of this and we can share with you what we’ve learned along the way to walk you through that journey to help you make wise choices, whether it be even looking into other insurance options, finding a lawyer will be best suited for you, or looking into other options like should I go on disability, should I file my VA claim, what else is out there for me. So we actually can help walk you through the whole process.

Right now I’m doing quite well. It’s been ten years now since the original diagnosis. I’m just so thankful for everything at this point.

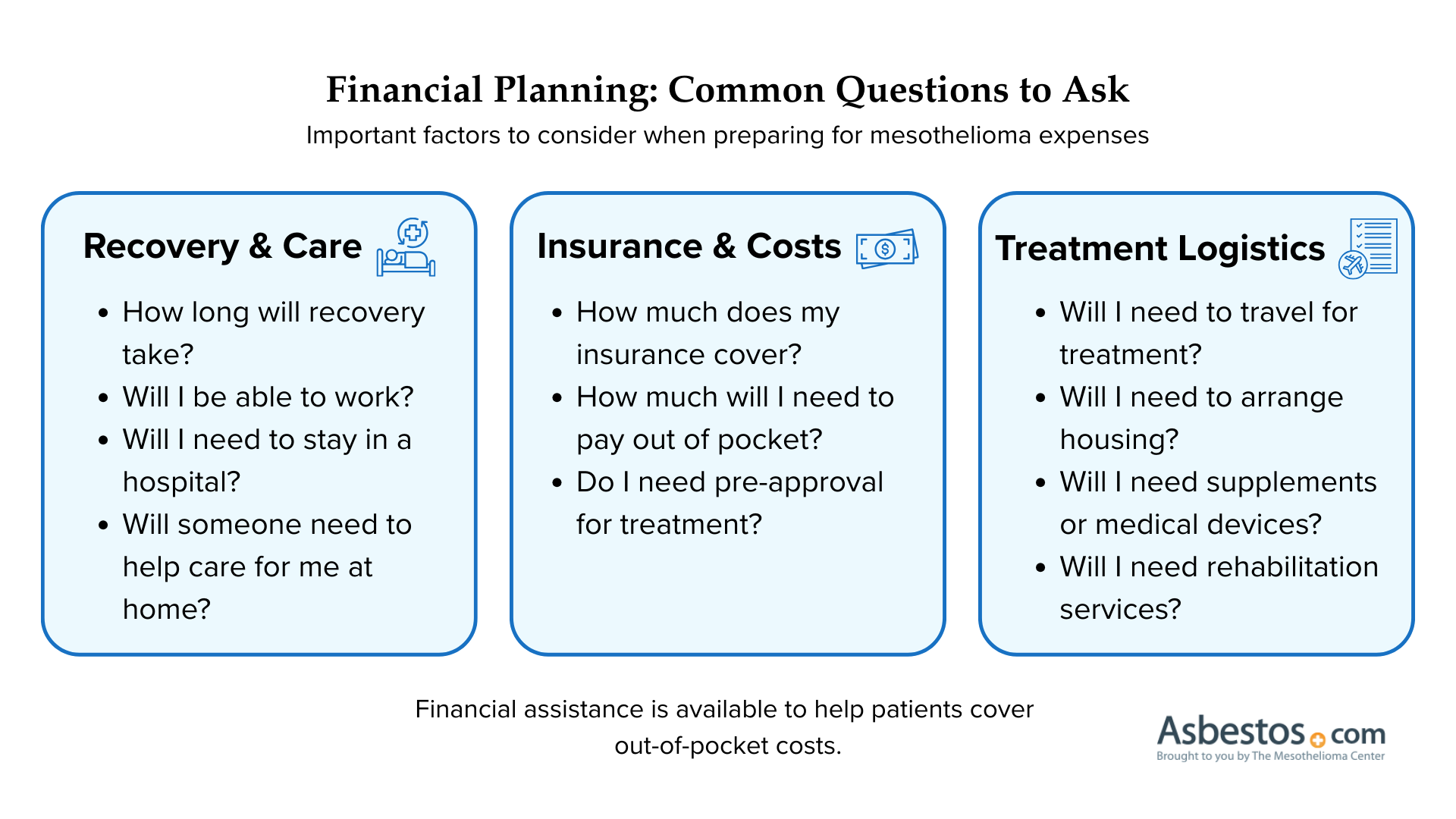

Get Organized and Ask Questions

Designate one or more trusted people to help with decision-making. They should know where to find your medical records, legal documents and contact information for doctors, mesothelioma lawyers and financial advisors. They may also need access to financial accounts and a power of attorney to make important decisions if needed.

Review your treatment plan and prepare for upcoming expenses. Consider questions about recovery, work, care needs, insurance coverage, travel and medical devices or supplements.

Common Questions to Ask

How long will recovery take? Will I be able to work? Will I need to stay in a hospital?

If I stay at home, will someone need to help care for me?

How much does my insurance cover and how much will I pay out of pocket? Do I need preapproval for treatment from my insurance company?

Will I need to travel for treatment and arrange housing?

Will I need supplements, rehabilitation or medical devices?

You may also find it helpful to speak with a billing administrator, social worker or patient navigator. Loved ones can call the insurance company to confirm coverage details. Always find someone who can give clear answers to financial or treatment questions.

Our team of Patient Advocates can also help you navigate insurance and your financial options. They can connect you with financial assistance as well.

$30B+ IN TRUST FUNDS AVAILABLE

Navigate Mesothelioma Treatment Costs

Discover financial assistance programs, insurance guidance, and veteran benefits to help cover your mesothelioma treatment expenses.

Take stock of resources available to you. Most Americans rely on health insurance to cover treatment for serious illnesses. Take a look at your health insurance coverage and explore what other options are available. This may include Medicare and Medicaid.

Many people receive their health insurance through their employer. But they can’t always continue working full-time during mesothelioma treatment. The Family and Medical Leave Act of 1993 may provide one solution. It ensures many American workers get 12 weeks of job-protected leave per year.

Tax deductions are another important resource for many mesothelioma patients. Medical expenses exceeding a certain percentage of a household’s income can be deducted from federal taxes. Caregivers may be able to take advantage of certain tax breaks as well.

Financial Help With Medical Bills

The cost of mesothelioma treatment can quickly overwhelm your available resources. Taking steps early can reduce stress and help ensure you have access to care.

Government programs and nonprofit organizations can help you cover travel for treatment, medical equipment, prescription drugs and other essential needs. Mortgage lenders, credit card companies and other creditors sometimes adjust payment schedules when serious illness presents special circumstances. You may also pursue compensation from asbestos trust funds, Department of Veterans Affairs benefits or mesothelioma lawsuits related to asbestos exposure.

Carefully track all expenses related to your mesothelioma diagnosis. These records can support your pursuit of compensation. Because mesothelioma claims have strict deadlines, looking into legal options early offers the best chance of protecting your finances.

Estate Planning

Financial planning for mesothelioma should also cover writing a will, making funeral decisions, naming beneficiaries for insurance policies and survivor benefits. These steps help protect your family and reduce confusion during a difficult time.

A mesothelioma diagnosis makes it especially important to complete legal documents without delay. Taking care of these matters early eases stress later and ensures your wishes are clear.

Financial Power of Attorney

This document appoints someone you trust as your agent or attorney-in-fact. This person will make financial or legal decisions for you if you become too ill to manage your own affairs.

A financial power of attorney typically allows your agent to handle tasks like banking, paying taxes or applying for government benefits on your behalf. Choosing the right person for this role is important.

Health Care Power of Attorney

This document names an agent or attorney-in-fact to make health care decisions for you if you’re unable to make them yourself. It may also let your agent talk with your doctors, access and share your medical records and ensure that you get the kind of care you want.

In some states, you can include a statement called an advanced directive, or a living will, in your health care power of attorney. This gives clear instructions about the types of care you want or don’t want, such as whether to receive life-saving treatments like CPR.

Will

A will provides directions for handling your estate after your death. It names an executor to settle your final affairs, such as paying debts and giving your property to loved ones. Without a will, a court decides how your property is divided.

If you have young children, you can also use your will to name a guardian for them. This ensures that someone you trust will take care of your children if something happens to you.

Recommended Reading

Your web browser is no longer supported by Microsoft. Update your browser for more security, speed and compatibility.

If you are looking for mesothelioma support, please contact our Patient Advocates at (855) 404-4592

Fact Checked

Our fact-checking process begins with a thorough review of all sources to ensure they are high quality. Then we cross-check the facts with original medical or scientific reports published by those sources, or we validate the facts with reputable news organizations, medical and scientific experts and other health experts. Each page includes all sources for full transparency.

Reviewed

Asbestos.com is the nation’s most trusted mesothelioma resource

The Mesothelioma Center at Asbestos.com has provided patients and their loved ones the most updated and reliable information on mesothelioma and asbestos exposure since 2006.

Our team of Patient Advocates includes a medical doctor, a registered nurse, health services administrators, veterans, VA-accredited Claims Agents, an oncology patient navigator and hospice care expert. Their combined expertise means we help any mesothelioma patient or loved one through every step of their cancer journey.

More than 30 contributors, including mesothelioma doctors, survivors, health care professionals and other experts, have peer-reviewed our website and written unique research-driven articles to ensure you get the highest-quality medical and health information.

About The Mesothelioma Center at Asbestos.com

Assisting mesothelioma patients and their loved ones since 2006.

Helps more than 50% of mesothelioma patients diagnosed annually in the U.S.

A+ rating from the Better Business Bureau.

5-star reviewed mesothelioma and support organization.

My family has only the highest compliment for the assistance and support that we received from The Mesothelioma Center. This is a staff of compassionate and knowledgeable individuals who respect what your family is experiencing and who go the extra mile to make an unfortunate diagnosis less stressful. Information and assistance were provided by The Mesothelioma Center at no cost to our family.

Asbestos.com. (2026, March 25). Financial Planning After a Mesothelioma Diagnosis. Retrieved May 20, 2026, from https://www.asbestos.com/treatment/financial-planning/

MLA

"Financial Planning After a Mesothelioma Diagnosis." Asbestos.com, 25 Mar 2026, https://www.asbestos.com/treatment/financial-planning/.

Chicago

Asbestos.com. "Financial Planning After a Mesothelioma Diagnosis." Last modified March 25, 2026. https://www.asbestos.com/treatment/financial-planning/.

Maximize Your Mesothelioma Settlement

The average mesothelioma settlement is between $1 million and $2 million. Find out if you qualify for a mesothelioma settlement.

Attorneys are available to discuss your case today

Over $30 billion available for asbestos victims. Time limits may apply

5.0 Rating160+ Google Reviews

A+ RatedBetter Business Bureau

20 YearsServing Exposure Victims

Most helpful, steered us in the right direction for treatment. Great source of information and support, the Center followed through on every one of our requests.

Because of their guidance, I was able to navigate getting my mother into MD Anderson when her case got put aside by mistake in all the COVID-19 craziness. Vanessa was amazing and I can’t recommend enough reaching out to them. I thought it was a gimmick to get you to hire a lawyer, but I was so wrong. They truly seemed to want to help meso patients and KNOW what you need to ask and do in order to get help.

Hearing the news about my mother's diagnosis was heartbreaking. I felt lost, I didn't know how I could help or where to seek the best medical care. I started researching specialists online and shortly after, Dr. Smart reached out to me. She has been extremely helpful and encouraging throughout this entire process. Even though we aren't located in her area, she has helped us get in contact and set up appointments with the best doctors/specialists nearby. She has always been available for any questions that we have, and she even sent us a binder full of helpful resources. The patient advocates are amazing and true to their title. Dealing with this process is not easy, but knowing that we have someone like Dr. Smart in our corner is reassuring and we are so grateful for her and The Mesothelioma Center.

My son Carlos was diagnosed with this terrible and unknown disease a few months ago. Thank God we found The Mesothelioma Center along the way, and Vanessa Blanco who provided us with information on hospitals and doctors who have been of great help. I am very grateful to them.

Extremely communicative and helped my dad get an appointment with one of the top centers in Philadelphia. I'm so grateful for this center. They assisted with information on nutrition, legal help, and scheduling appointments. Special thanks to Danielle!

Danielle DiPietro was an invaluable resource for me. Her suggestions and recommendations guided us towards stellar practitioners in our area. Without her advocacy, I feel we would have been receiving less-than-optimal medical and legal care for mesothelioma. Receiving the diagnosis was a shock and I felt lost initially. I wish everyone could take advantage of this FREE assistance.

I was very grateful and appreciative of Dr. Smart from The Mesothelioma Center. She was very helpful to my husband and me. She educated and walked us through the steps, and suggested ideas and questions to ask his doctors. She also provided me with a lot of information that I can read and educate myself about this illness. We need more people like Dr. Smart, who is very educated and you can tell she enjoys the work that she does by the way she assisted my husband and me. We thank the Lord and are grateful that we met Dr. Smart from The Mesothelioma Center.

In January of 2016, my husband was diagnosed with peritoneal mesothelioma. Our first reaction was: what is this and what can we do? He was diagnosed by an oncologist and was scheduled to start chemotherapy. When we arrived home that day, I googled mesothelioma and discovered The Mesothelioma Center had a form to fill out to request additional information. I filled it out and within an hour, I received a phone call from Karen Selby from The Mesothelioma Center asking if I needed any help. Karen was and still is my lifeline. She located a doctor at the Cleveland Clinic who performed surgery and HIPEC on peritoneal mesothelioma patients. My husband was scheduled with an appointment and his surgery was performed on March 3, 2016. He continued with follow-up appointments with the oncologist until a friend of ours passed away from it in 2017. Immediately I sent Karen an email asking if she knew any mesothelioma specialists at the clinic, and of course, I got a prompt response back with a name. Everything was going well until the last CAT scan, which showed it returned. He is now doing chemo and has his next CAT scan scheduled for the end of March with a follow-up for the results with the mesothelioma doctor. Without Karen, I am not sure my husband would still be here. She provided me with so much information along with help in various ways, too numerous to even mention. Thank you to all those who are there to help us.

Missy Miller has connected mesothelioma patients with top doctors since 2010. Through the partnerships she has built across the U.S., Miller makes sure every patient is seeing the right professionals to improve their prognosis. She guides families on where to turn for medical, financial and emotional support.

Fact-checked and verified content:

Our fact-checking process begins with a thorough review of all sources to ensure they are high quality. Then we cross-check the facts with original medical or scientific reports published by those sources, or we validate the facts with reputable news organizations, medical and scientific experts and other health experts. Each page includes all sources for full transparency.

Please read our editorial guidelines to learn more about our content creation and review process.